Now is a great time to work with i-squared! You will get a high-touch, well researched, customized portfolio. All done with a client first approach, integrity, and independence. Feel free to reach out.

As a reminder:

*i-squared named Five Star Advisor for 2023, 2024, 2025, check out this short video: CLICK HERE

*i-squared ranked Top 20 Wealth Management Firm in the US, click HERE

*Now offering a customized AI Opportunities Strategy, AI looks like the next mega-cycle in investing. McKinsey estimates that it could be worth $4.4 trillion annually. Marc Andreessen says, " AI is quite possibly the most important – and best – thing our civilization has ever created, certainly on par with electricity and microchips, and probably beyond those." please reach out for more details on AI Strategy

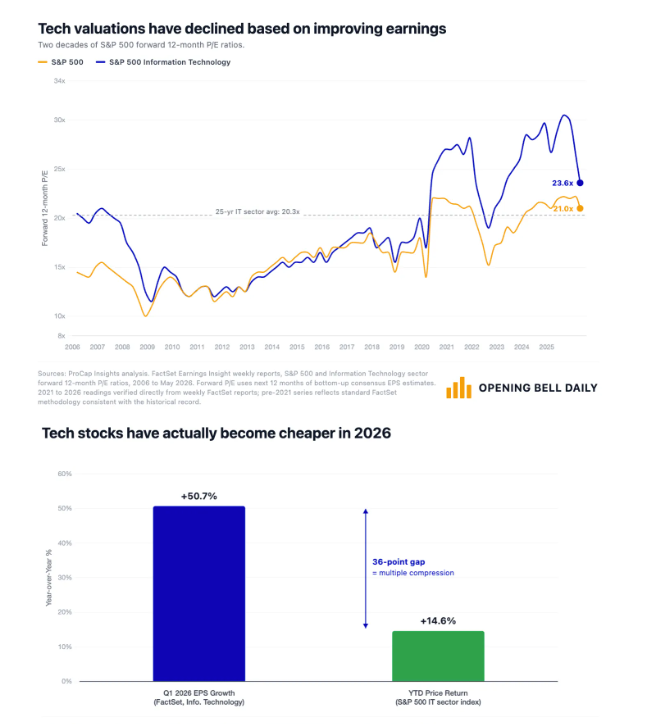

This is not a stock market bubble; this is a historic value transfer from the losers to the winners of AI. It is very hard to argue that it is a bubble when the multiple for tech stocks is down for the year. The forward 12-month P/E for the S&P 500 tech sector now sits at 23.6x, down from its peak above 30x last fall. The multiple is back to where it was six years ago. The tech multiple is lower, despite margins at an all-time high, nearing 30%. To put this in perspective the forward multiple during the dot.com era was 60x, with many leading names north of 100x. Cisco reached 210x the dot.com era! Nvidia trades at 17.0x forward earnings, cheaper than Coca-Cola at 23x, which grows one-tenth as fast. The AI specific names trade at just a 0.6x PEG ratio, compared to 3.3x for consumer staples, 1.8x for utilities, 1.6x for the S&P ex-AI, and 1.1x for the S&P. The gains this year have not kept up with tech's astounding 50.7% earnings growth. The AI specific names are expected to grow 55% this year, compared to 22.1% for the broader S&P. The market is rewarding what is growing and expanding margins.

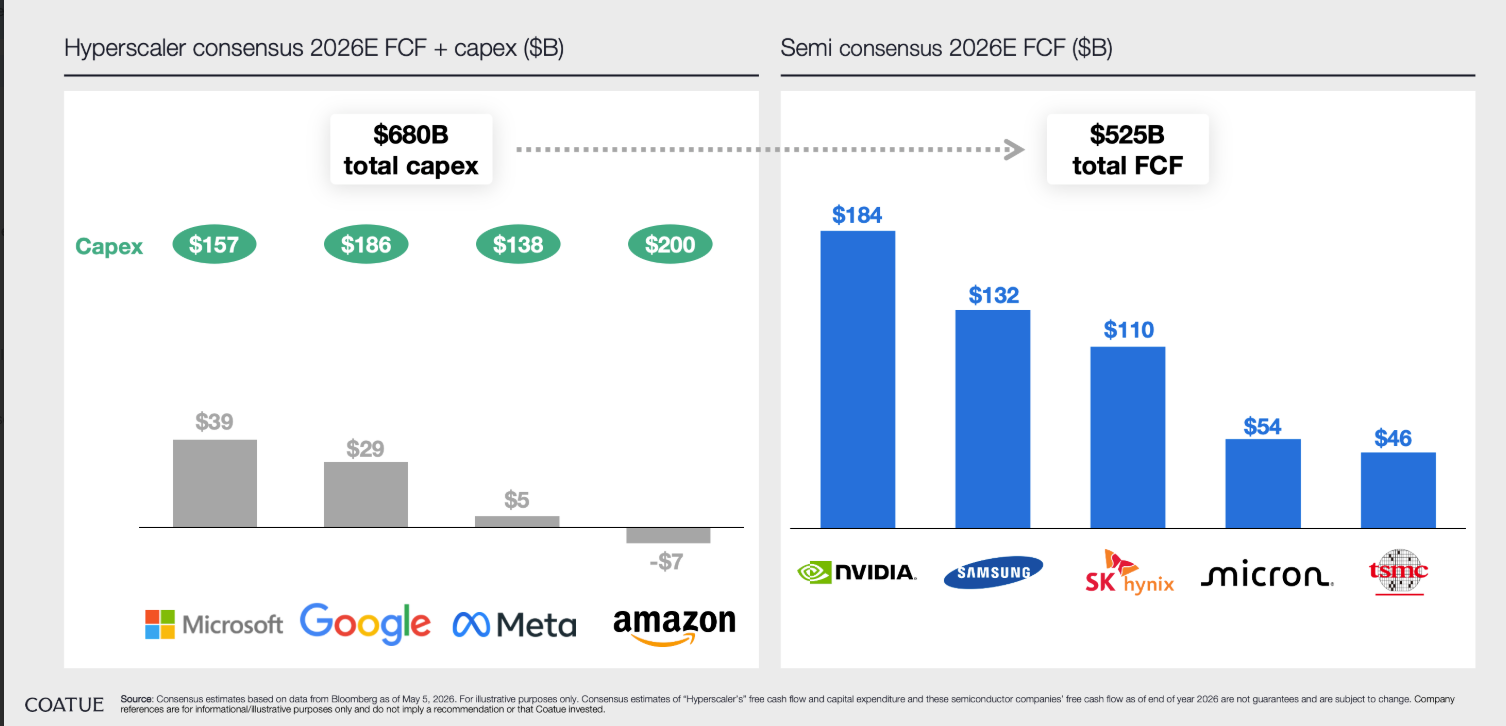

There are two transfers of value that are occurring. The first is from the hyperscalers that are spending on cap-ex to the beneficiaries of this cap-ex. This is mostly AI semiconductors and infrastructure names. The hyper-scalers will spend $680bn on cap-ex this year. AI-semiconductors are expected to have $525bn in free cash flow. The market impact for the hyperscalers is multiple contraction. The combination of lower free cash flow, lower buybacks, and a shifting business model from capital-light to capital intensive is driving this re-valuation. For instance, Microsoft’s multiple is down eight multiple turns this year, Meta is down six turns, and Amazon is down 5 turns.

The second transfer occurring is from AI-losers such as software companies, financial data providers, private equity companies, consulting companies, travel-booking companies to AI-winners such as semiconductors and infrastructure names. Over the last year the former group of companies are down anywhere from 20% to over 50%, while AI winners are up north of 100%. Since the introduction of ChatGPT, software has gone from 14% of the S&P to under 9%, while semiconductors have gone from 7% to nearly 20%. Other AI-losers and hyper-scalers account for the additional donation to semiconductors. The correlation pre-ChatGPT between software and semiconductors was nearly one, that has now fallen to just 0.30. The market is revaluing AI-losers as their terminal value is increasingly uncertain and transferring that value to winners.

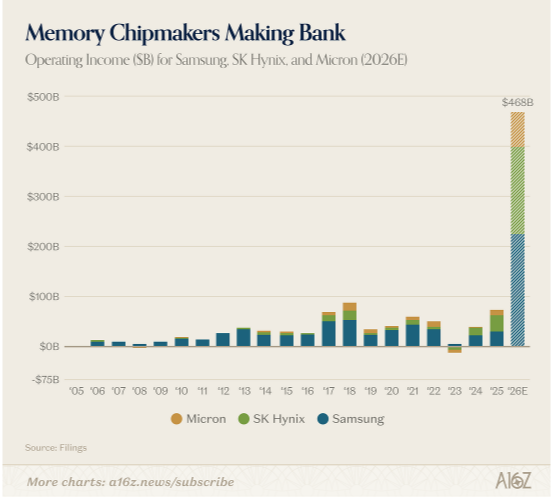

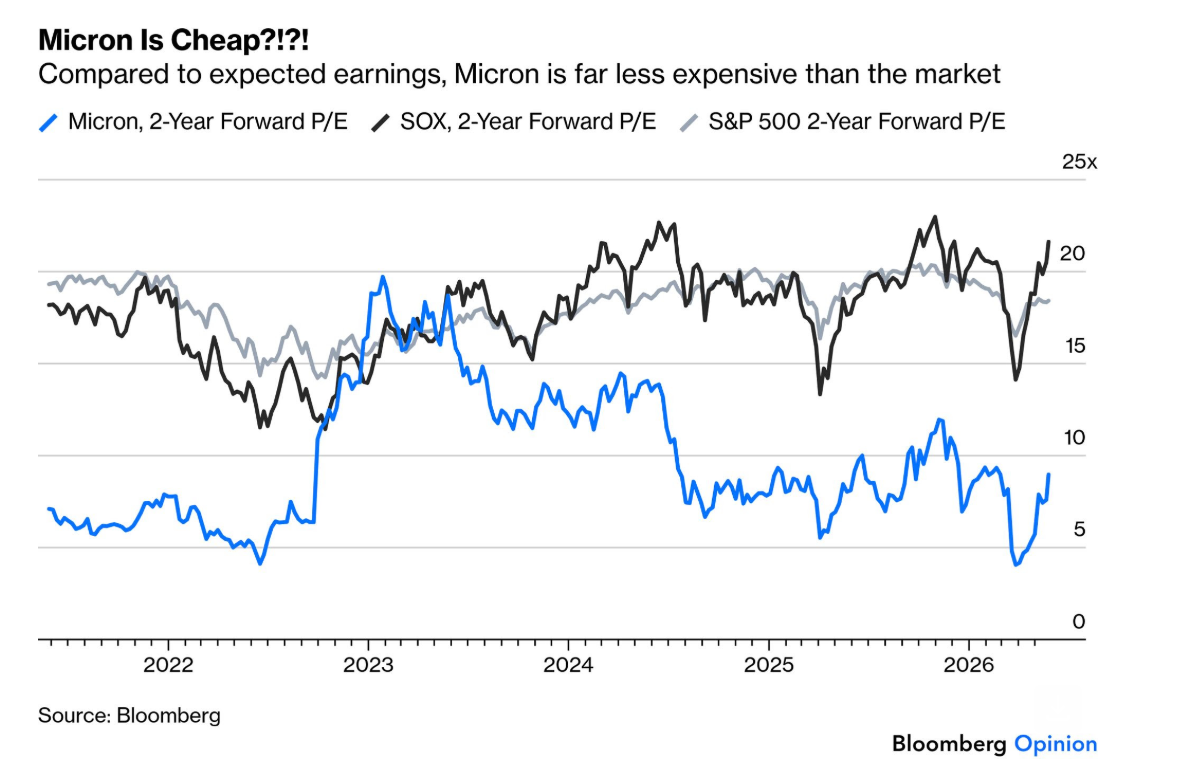

One of the key beneficiaries of this value transfer is the memory stocks. They are up a lot this year, but their operating earnings in 2026 are expected to sextuple! Micron earned more in the first quarter of this year than in any single year prior to 2025. It had nearly double the operating income of Walmart last quarter. Margins have expanded from 20% to 74% in the last two years. The multiple is 8.8x and the PEG is well below 1.0x, not exactly demanding. Memory has been historically commoditized, so the multiple deserves to be low for now. That said, we have a historic shortage and it does take years to bring on new capacity. Plus, hyperscalers are signing 5-year agreements, compared to the industry standard of a year. Samsung said that, “based solely on the demand currently received for 2027, the supply-to-demand gap for 2027 is set to widen even further than in 2026.” In a bubble market the terminal value would be expanding, that is not occurring. The market is barely keeping up with earnings growth and margin expansion. It is waiting for more confidence that a highly cyclical industry is transitioning to a less cyclical one before expanding the multiple.

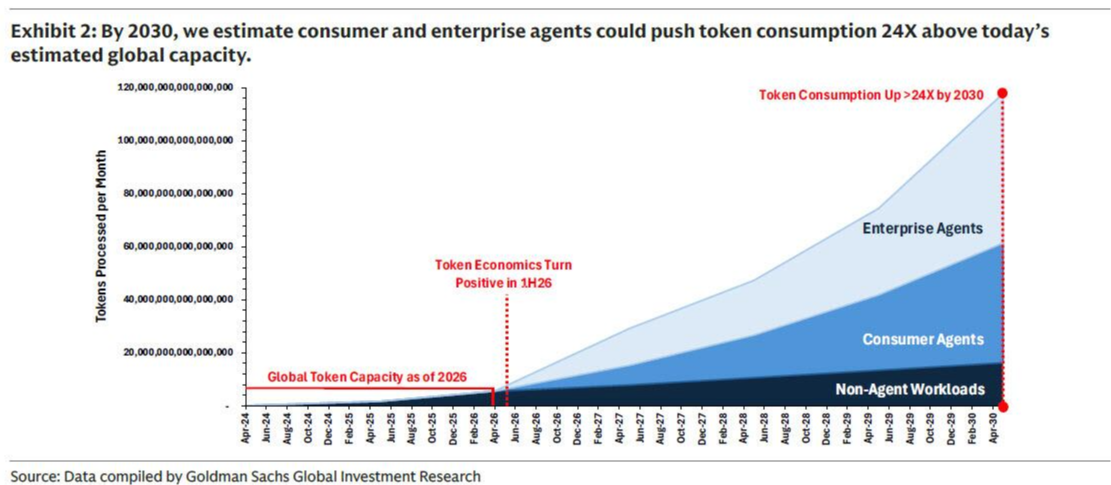

The numbers AI-related companies are reporting are unprecedented. At an event in May, Anthropic’s CEO said that they saw 80x growth in the first quarter! 80x! Demand for agentic AI is driving unprecedented demand for compute. Nvidia’s CEO said, “we'll have hundreds of billions of agents ... we're going to need a lot more CPUs ... [AI] demand is much greater than overall capacity ... we're at the beginning ... decade or maybe more ... supply chain is more than doubling every year." Citi estimates that the CPU total addressable market could expand from $29.3 billion in 2025 to $131.5 billion in 2030, or a 35% compound annual growth rate. The demand for compute will only increase as physical AI, robotics, and self-driving cars are more prevalent. Less than 1% of the population uses AI to its capabilities and we are already short compute. Google in the past year has gone from processing 480 trillion tokens to 3.2 quadrillion tokens. Goldman estimates by 2030, token consumption will rise to 120 quadrillion tokens per month!

For investors, expect a lot more dispersion as the market re-prices both winners and losers. There is an 85% spread between what the top quintile stock is doing versus the bottom. There have been many days in recent weeks when the S&P has hit new highs, with more stocks down than up and more 52-week lows than highs. Only 4% of S&P stocks are at new highs. The winners are winning big, and the losers are losing big, which is leading to offsetting results for many passive investors. 222 of the 500 S&P stocks are more than 20% off their high, and 109 are more than 40% off. The gains for the winners will not come easy, there will be periodic violent volatility events to shake-out weak hands. Using technicals and having conviction in fundamentals will be critical during those times. The combination of value transfer, volatility, offsetting positions, and dispersion means that it is probably better to be a stock picker than an index investor. An index investor is stuck with too many losers.

Looking forward the market will focus on the latest in AI, geopolitics, rates, and a new Fed Chair.